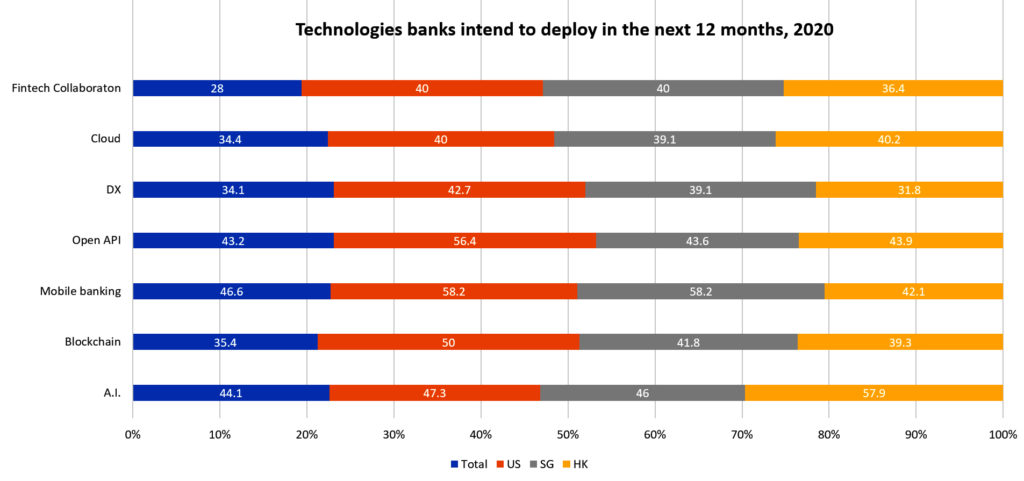

A global survey released by Finastra reveals that Hong Kong financial institutions are leading markets including Singapore, the US and the UK in their intentions to deploy Artificial Intelligence (AI).

Finastra research found that 58% of 107 financial institutions in Hong Kong are looking to deploy the technology in the next year, at least 11% higher than any other market surveyed. It also found that 36.4% of financial institutions in Hong Kong view fintech collaboration as a contributor to their success.

That banks in Hong Kong are on some path towards the use of AI (if not already having such tech in production) is just plain being ignorant. At the same time, any concerted effort on the part of the industry to tap the technology would be just plain lying.

As Sneha Kapoor, senior technology analyst and consultant, IDC Financial Insights for Asia-Pacific, explained: “Most of the AI initiatives by FSIs in Asia/Pacific have been ad hoc pilot projects or a part of fragmented, siloed experiments by various product units, functions, and business–IT teams throughout the enterprise. The concept of “AI at scale” is still missing.”

She revealed that only a very few institutions are now articulating how AI needs to be a part of their core strategy and how AI and the class of technologies that constitutes it broadly support organizations’ long-term goals.

AI motivations

Victor Alexiev, director, APAC head for Citi Ventures Programs & Strategic Partnerships, Institutional Clients Group at Citi explained that there are many ways in which AI and advanced analytics in general can create value, from extracting insight from non-structured data sets (text, voice and image) to automating repetitive tasks.

AI motivations

Victor Alexiev, director, APAC head for Citi Ventures Programs & Strategic Partnerships, Institutional Clients Group, cited three areas where AI is creating value for the bank:

- Efficiency gains: many operations process rely on a maker-checker model, usually involving multiple handlers between systems and humans. Removing manual touchpoints that involve subjective judgement via basic automation (RPA) or more intelligent judgement models helps save time and reduce the error rate.

- Risk reduction: the volume of individual decisions and transactions taken every second in a large, global enterprise like Citi is extensive and here is where AI surveillance is useful. Citi is already leveraging various outlier detection and pattern recognition (e.g. voice identification) tools to protect its clients and manage risk. But with a rapidly evolving playing field, staying abreast and adding more monitoring tools is critical in for good risk management.

- Better utilization of data assets: much of the data that flows through enterprises are not utilized. Building a better understanding of our customers and employees to improve our relationship with them is one domain of interest. Bringing in the alternative, streaming data sets and blending them with our own to create insights in real-time and support decision-making holds vast potential. As technology improves, the intelligent, data-driven, enterprise will be the norm.

Use cases

“We believe that the investigation into AI is deemed to have a high need for localization to ensure that algorithms used by institutions are sufficient and fit for each Asia/Pacific market. The localization of AI is crucial for a long list of AI use cases: from chatbots and recommendation engines (to capture local nuances and slang) and credit decisioning (behavioural scoring despite thin files in developing markets) to fraud analytics (to understand unique transaction patterns),” elaborated IDC’s Kapoor.

Andy Nam, chief information officer for Greater China North Asia at Standard Chartered Bank (SCB) called out the following use cases as the responsible application of AI and machine learning:

- In commercial banking, SCB relationship managers have access to insights that leverage transaction patterns and usage trends to predict solutions their clients are likely to need in the future.

- In retail banking, SCB is using machine learning and alternative data sources for market campaign that are hyper personalised for individual customers across multiple countries. To enhance customer service and promote customer self-service, SCB introduced Stacy in Hong Kong – a chatbot that is powered by Kasisto. With the AI engine inside, SCB is able to continuously refine the service offering to the customers. Chatbot usage has increased by 60% year-on-year so far, with containment and accuracy rates above 80%.

- In corporate banking, SCB uses data to understand the foreign exchange and payments activities of its clients.

- SCB’s Financial Crime Compliance team has partnered with Silent Eight, a Singapore-based AI start-up, to use machine learning to automate some of the work in investigating financial crime alerts.

“We have been using data-driven insights to improve the way we serve our clients. With the advancement in AI, we are exploring applications of AI/ML to better these processes and services within the guidelines of responsible AI,” Nam explained.

Future trends

IDC Financial Insights expects that by 2022 more than 50% of Asia/Pacific financial services institutions (FSIs) will invest in one or more AI technologies. Majority of projects will focus on three objectives: transform the customer experience, optimize operational efficiencies, and create new revenue streams.

Kapoor cited two factors that will contribute to successful adoption of AI: how an institution readies itself in embracing AI and the capability of the solution to deliver expected results.

For the first element, institutions need to think and prepare itself for five key dimensions: strategy and sponsorship; process identification and optimization; people and change management; scalable infrastructure; and data and model life-cycle management. The advancement on each of these dimensions will determine how an institution perceives and utilizes AI for success.

The second element will define the capability of the solution (a solution could be proprietary either developed by the in-house team or developed by external partners) to deliver on the expected results. Even though most of the institutions may choose to spend more time and efforts on choosing the most appropriate solution, the competence of a solution to deliver the best quality outcomes, advice, and decisions will also depend on the institutions’ ability to address their own internal readiness for AI.

AI roadmap

Citi’s Alexiev listed a number of important considerations when building an intelligent enterprise. In the case of Citi, ethics and compliance, data, tools and inftrastructure, as well as practical use cases all carry weight when evaluating future solutions.

But not everyone has an expansive strategy when it comes to emerging technologies. Certainly an organisation as old as banks have legacy baggage they need to contend with when evaluating their way forward particularly around new and still evolving technologies.

Kapoor noted that many of the FSIs in the region are not digital-native and are stuck with traditional ways of thinking and working.

“They still do not consider AI as part of their core, enterprisewide strategy, and as a result, it is being implemented as part of a fragmented, siloed approach without any long-term road map to achieve scale,” she added.

Tech must be involved – establishing centres of excellences (COEs), where cross-functional teams collaborate will be key. She pointed to the formation of interdisciplinary teams, many of which are agile development teams with collaborations from vendors, service providers, product teams, technology and operations, sourcing teams, innovation teams, and other teams.

“These collaborative practices will bring together diverse skills and experience from within the institution to build more effective solutions,” she concluded.

AI’s collaborative and evolving nature suggests different business models will continue to emerge as organisations discover what they could do with the technology. The path to discover is also paved with options. These can range from a fully in-house, custom-built approach to a more modular approach using pre-built solutions and tools, or to a fully outsourced approach solely relying on third-party vendors.

As Omdia pointed out the widespread availability of programming platforms and tools, as well as cloud-based infrastructure, has led to a major shift in the market.

“Enterprises do not need to lock into a single AI vendor; they can hire data science teams and engineers to develop, train, and run AI models from scratch. Yet, a significant portion of the enterprise market has neither the skill nor the budget to develop AI from scratch. As such, many vendors sell pre-built AI solutions or tools, and consultants and contractors can customize off-the-shelf AI. No single business model is going to be right for all enterprises looking to deploy AI. There will be room for many approaches and vendors for the foreseeable future,” noted the analyst.

Omdia forecasts annual AI software revenue to increase from $10.1bn worldwide in 2018 to $126.0bn in 2025.