The uncertainty in the future economic viability of the telecoms business is making change an immediate necessity. As mobile operators struggle with an identity crisis, their vendors have been acquiring new strengths to tackle the potential with digital through M&A e.g., Ericsson acquired Vonage, and IT players have been encroaching into the network space e.g., Microsoft acquired Metaswitch, for network capabilities to further tap on the enterprise opportunity.

Only a handful of mobile operators e.g., Singtel, Vodafone and T-Mobile, are leading the way with 5G solutions for enterprises. 5G solutions are coming out of the boxes to make it easy for enterprises to adopt but more success with 5G is needed.

The industry cites cost and monetisation as challenges faced with 5G. However, the business case could still make sense at a high cost if monetisation was not an issue. Therefore, monetisation may be the bigger problem, not cost but cost still needs to be managed. New innovative business models need to be crafted to re-engineer cost and reduce risk.

Approach to building infrastructure

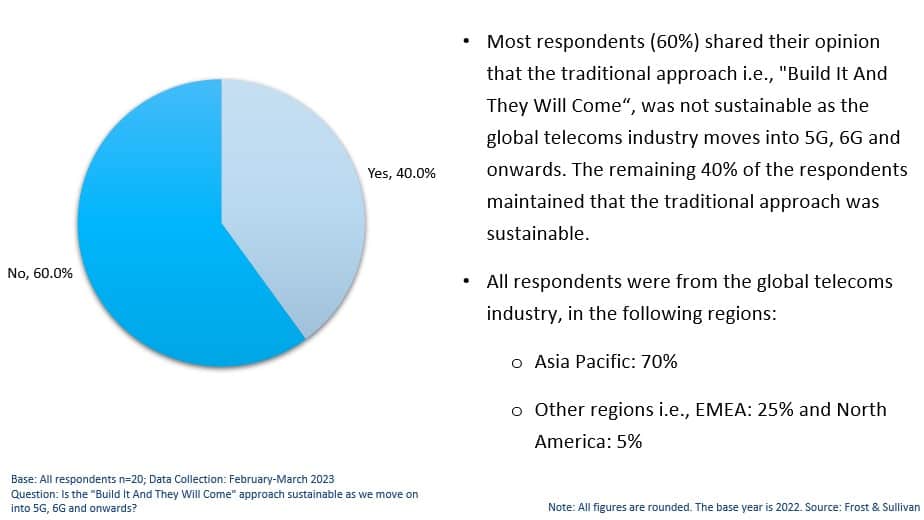

A 2022 Frost & Sullivan survey found that 60% of respondents cited that they do not believe the “Build it and they will come” approach will be sustainable from 5G onwards. Mobile operators and their regulators need to consider new approaches to improve future prospects.

If there is a need, 5G will be embraced. Indeed, 5G is finding a place in some of the most automated industries e.g., in existing semiconductor factories in Taiwan, driven by the use of augmented reality and artificial intelligence.

The reality is that some companies and some parts of the industry are moving faster with 5G because there is an exact fit for the need being addressed but others require some development for there to be fit.

The success of a few companies that are taking a different approach and achieving better outcomes e.g., Rakuten Mobile, signals time for a review of the relevance and effectiveness of global alignment. Competing global IT players can craft and execute monetisation strategies faster than the global associations that bring together more than 750 mobile operators.

Beyond connectivity, the need for end-to-end integrated services cannot be met without greater collaboration. The legacy mentality of control needs to give way to trust as the future growth of the telecoms industry depends on how well companies can collaborate.

Of the many partnerships that have been announced, many are collaborations with companies that do not compete. Part of the reason for this could be attributed to collaboration skills being rare amongst the telecoms industry workforce, where a large majority of workers still comprise of men and the industry struggles with discrimination.

Another reason is that tapping on the opportunity requires companies to be more open, which is still not something that is intuitive for companies, especially in the telecom industry.

The telecoms industry faces a skillset shortage that hampers the adoption of new emerging technology and new practices. Attracting top talent is a challenge as the industry is no longer a high-growth industry.

The incorporation of automation in parallel further adds complexity as mobile operators need to find the right balance between human touch and automation. Finding the way forward with culture and talent needs to fall back on a clear strategy for business transformation.

The industry understands change is necessary but achieving change is an uphill challenge. Up until recently, decisions have been for the short term. The business transformation that is necessary at this juncture is meant for the long term, where clarity is elusive, and success is not guaranteed. This increases the difficulty in getting everyone on board, investors and customers alike. However, the future of the telecoms industry is at stake should effective change not be made an immediate strategic imperative on mobile operator CEO agendas.