ResearchAndMarkets forecasts that the embedded finance industry in the region is expected to grow by 39.7% on an annual basis to reach US$120,534.9 million in 2023.

"The embedded finance industry is expected to grow steadily over the forecast period, recording a CAGR of 29.0% during 2023-2029. The embedded finance revenues in the country will increase from US$120,534.9 million in 2023 to reach US$397,298.2 million by 2029." ReseachAndMarkets

What's driving embedded finance? For traditional financial services, it is a growing threat that well-executed fintech-led companies have successfully unbundled financial services and eaten into the ability of incumbents to cross-sell and upsell.

The 2023 FIS Global Innovation Report revealed that 55% of non-financial businesses surveyed in Singapore say they are already offering or developing embedded finance services.

Finastra's regional head of payments, Dheeraj Joshi, says embedded finance is the integration of financial services – such as payments, insurance, loans, etc – into a company’s services. He cites the example of how payments are built into ride-sharing apps, such that users do not have to input their payment details for each ride.

"Other increasingly common examples are e-commerce platforms offering BNPL (Buy Now Pay Later) options during checkout, or airlines offering travel insurance during the booking process," he elaborated.

Kanv Pandit, group managing director for banking solutions in APAC at FIS says embedded finance is a blurring of the traditional lines between financial and non-financial companies, with technology advancements making it easier than ever for companies from all industries to layer in financial capabilities to their products and enhance their customer propositions.

New partnerships

Mayur Tanna, the CIO of TransformHub, explains that typically, what is behind the digital platforms driving embedded finance are not banks, but software firms that collaborate with technology companies and banks to integrate financial products into a unified, convenient, and user-friendly experience for the customer.

"We are therefore seeing a novel form of collaboration between banks, technology vendors, and distributors of financial products via non-financial channels, which is essentially a new value chain to address market demands," he continued.

The democratisation of financial services

Tanna is quick to point out, however, that embedded finance won’t mean the demise of traditional banking, but it will increase competition in the fintech landscape, drive innovation, push traditional banks to evolve and offer new products and services, and spur partnerships with fintechs and technology providers.

"By making financial services more affordable and accessible, embedded finance will help democratise the industry and benefit the unbanked and underbanked by providing them with services they would otherwise not be able to enjoy," he elaborated.

Misconceptions about embedded finance

The other finance-focused disruption that has risen to the consciousness of traditional financial leaders in recent years is banking-as-a-service (BaaS).

Deloitte defines BaaS as the provision of banking products and services through third-party distributors.

"Through integrating non-banking businesses with regulated financial infrastructure, BaaS offerings are enabling new, specialised propositions and bringing them to market faster."

Deloitte

You will be forgiven for thinking BaaS is the same as embedded finance. Commenting on the misleading practice of interchanging the two, Pandit explains that BaaS is taking bank functionality, compartmentalising, or grouping it, and then individually offering these functions to non-financial companies.

"To meet the rising demand for embedded finance, BaaS is how existing financial institutions are describing their offerings —bundled, often white-labelled, or cobranded - so that non-banks can use them to serve their customers," writesZac Townsend, an associate partner at McKinsey.

As Zilvinas Bareisis, head of retail banking and payments research at Celent, puts it: "Embedded finance is the “what”, and BaaS is often, although not exclusively, the “how”."

In other words, "BaaS is a concept enabling digital banks and other third parties to connect with regulated banks via APIs, allowing them to build financial services offerings on top of traditional banks’ regulated infrastructure," calls out Finastra's Joshi.

Technologies behind embedded finance

Tanna noted that underlying the success of embedded finance is the use of APIs or application programming interface– software that provides programmatic access to service functionality and data within an application or a database.

Gartner explains that an API can be used as a building block for the development of new interactions with humans, other applications, or smart devices. Companies use APIs to serve the needs of a digital transformation or an ecosystem and start a platform business model.

TransformHub's Tanna concurs adding that financial APIs are the “glue” that enables links to be established between banks, other financial institutions, and non-bank institutions. He goes on to explain that API integration connects applications and enables data exchange, while financial API interfaces allow secure third parties to access a financial institution's platform.

With these technologies, businesses can effortlessly tap into embedded finance providers and provide customers with convenient, seamless, and flexible transaction experiences," he added.

How CIOs can get ahead of the game

Tanna explains that embedded finance is an example of digital transformation that has real-world business impact. It also underscores the CIO’s contribution to business competitiveness.

Mayur Tanna

"To get ahead, CIOs need to tie digital transformation to business functions with a clear impact on ROI. Becoming digital is not an end game but an ongoing, incremental, and iterative journey, and for the CIO, the goal is not only to add value to the business but transform the business and set it up for continued success."

Mayur Tanna

When evaluating the embedded finance opportunity

While embedded finance can enable non-financial brands to diversify their offerings and increase their lifetime value, Pandit warns that CIOs consider whether embedded finance adoption is truly necessary to improve the customer experience or create unnecessary barriers due to poor integration.

"Investing for the sake of investing can prove detrimental for a company. That is why leaders must take a wide look at their company and pinpoint exact areas where embedded finance can help their business grow," he concluded.

Questions to ask vendors

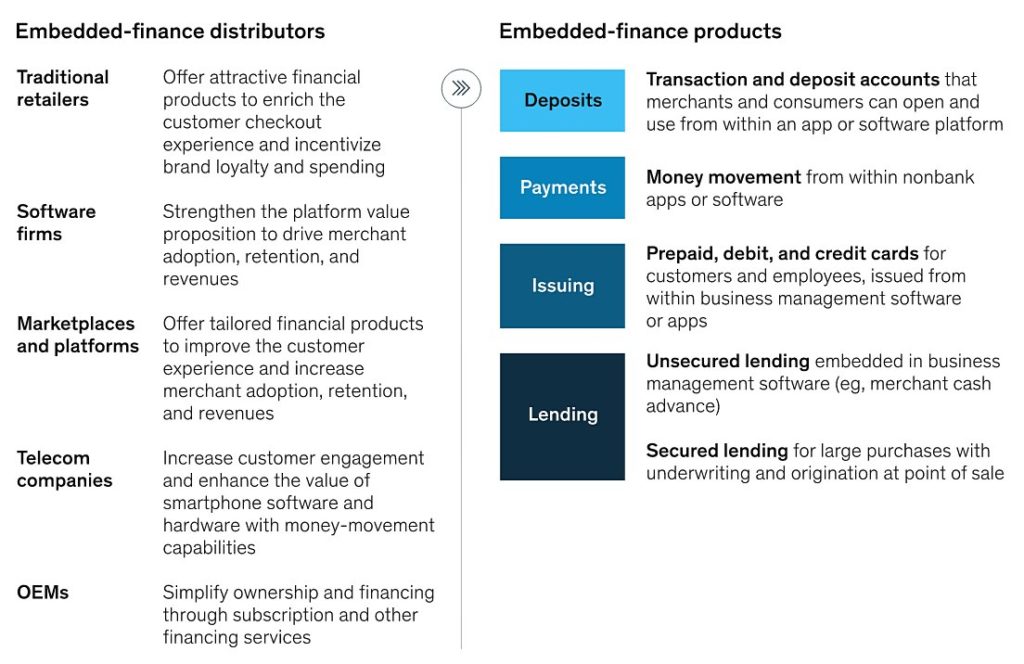

McKinsey notes that embedded finance is likely to emerge in any environment in which a critical mass of end customers (consumers or businesses) has frequent (often daily) digital interactions with the operator of the digital platform, which we refer to as the “distributor” of embedded finance.

Figure 1: Where demand for embedded finance is growing

Source: McKinsey analysis, 2022

"The embedded-finance product portfolio is likely to expand further as customer-onboarding and product-servicing processes are gradually digitised and real-time risk analytics and services grow more sophisticated."

McKinsey

Pandit says a key question is how should embedded finance solutions be integrated with existing core capabilities already in place. He adds that the shift to platform-based business models and an ecosystem set-up provides firms with various opportunities.

Kanv Pandit

"The foundation of much of the potential embedded finance innovation will be the increasing use of APIs that enable the sharing and co-creation of solutions between financial institutions, non-financial players and third-party providers." Kanv Pandit

Kanv Pandit

"These collaborations will enable companies to explore alternative products, methods of service delivery and even revenue models while providing a vastly improved and seamless experience for the end customer," he continued.

Integration challenges CIOs must face

Pandit cautions that while there are clear benefits to consider with API delivery, this can also present a security challenge. "The trend towards embedded finance promotes growing interconnectivity, which unfortunately can create more points of vulnerability. Technology innovation with APIs must be carefully aligned with security processes and procedures for firms to continue their role as trusted advisors to their customers," he continued.

Finastra's Joshi concurs adding that embedded finance requires seamless integration with the underlying technology infrastructure of existing platforms. This needs compatibility and smooth data flow between disparate systems, which can be complex, especially when dealing with legacy systems or multiple third-party providers.

"CIOs must also think about performance and scalability, as embedded finance should be able to handle a high volume of transactions and accommodate growing demand as users to the platforms increase," he continued.

Dheeraj Joshi

"The integration must be designed to handle peak loads, ensure minimal downtime, and provide real-time responses to users. Scaling the infrastructure, optimising database performance, and load testing the integrated system is essential to maintaining a seamless user experience."

Dheeraj Joshi

He went on to explain that embedded finance also requires a collaborative mindset, as a collaboration between different entities such as the platform provider, financial institutions and technology vendors are expected.

"Establishing and managing partnerships requires effective communication, agreement on technical specifications, legal considerations, and defining responsibilities. Aligning the goals and requirements of all stakeholders can be a challenge, especially when dealing with multiple parties across different organisations," concluded Joshi.

Allan is Group Editor-in-Chief for CXOCIETY writing for FutureIoT, FutureCIO and FutureCFO. He supports content marketing engagements for CXOCIETY clients, as well as moderates senior-level discussions and speaks at events.

Previous Roles

He served as Group Editor-in-Chief for Questex Asia concurrent to the Regional Content and Strategy Director role.

He was the Director of Technology Practice at Hill+Knowlton in Hong Kong and Director of Client Services at EBA Communications.

He also served as Marketing Director for Asia at Hitachi Data Systems and served as Country Sales Manager for HDS’ Philippines. Other sales roles include Encore Computer and First International Computer.

He was a Senior Industry Analyst at Dataquest (Gartner Group) covering IT Professional Services for Asia-Pacific.

He moved to Hong Kong as a Network Specialist and later MIS Manager at Imagineering/Tech Pacific.

He holds a Bachelor of Science in Electronics and Communications Engineering degree and is a certified PICK programmer.