A Gartner survey of 403 supply chain leaders in Q2 2022 revealed that 95% are evaluating or executing changes to their China sourcing and manufacturing strategy, and 55% of those already acted on their plans.

Hybrid regional model with local and regional elements embedded in global networks are emerging as the most popular option, with 40% of respondents see APAC not only as a supply base, but as an end market.

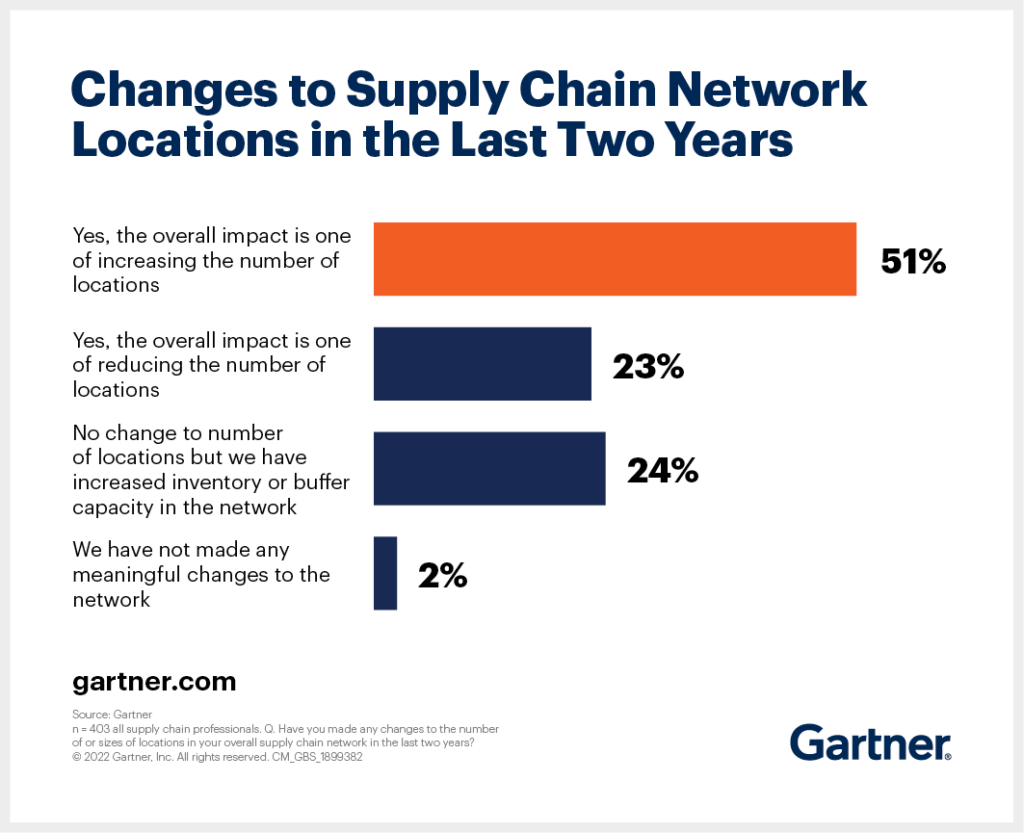

The survey also noted that 74% of supply chain leaders made changes to size and number of locations in their supply chain network in the past two years. Up to 51% of respondents said they increased the number of locations (see Figure 1).

As constraints, inflation, sustainability goals and national industrial policies put global supply chains under pressure, chief supply chain officers (CSCOs) are adapting their networks to fit this new environment.

“There’s clearly a supply chain redesign underway, but not everyone is moving in the same direction or even to the same extent,” said Kamala Raman, VP with the Gartner Supply Chain practice.

“Supply chain leaders have been modifying networks in a number of ways, be it with expansions, consolidations or simply modifications to buffers – which are more reversible than footprint decisions.”

Figure 1: Changes to supply chain network locations in the last two years

The resulting networks span a variety of operating models. Among respondents, 28% now describe their network as a hybrid regional model – a combination of local or regional elements in a global supply chain network. This is closely followed by global models with regional final assembly (23%) and local-for-local networks (22%).

“While the range of scales and approaches is wide, supply chains are undoubtedly on the move. Over half of participating organisations report making changes to manufacturing and supplier networks supporting at least 20% of revenue,” Raman added.

Asia remains valued as both supply bases and end markets

In supply chains with a presence in China, change is afoot as well. In total, 95% of survey respondents are evaluating or executing changes to their China sourcing and manufacturing strategy, and 55% of those already acted on their plans.

However, the survey data does not show strong signs of large-scale nearshoring to developed markets. Supply chain organisations are examining A China Plus One approach that leaves most of the China-based network intact and places net new additions in other markets, or a diversification strategy that still holds significant sourcing or manufacturing in China.

As a result of the diversification away from China, many countries in the rest of Asia are profiting from net new foreign direct investment.

Regional trade pacts flourish

There are also regionalised Asian networks emerging which are driven by coordinated industrial policies, such as the Regional Comprehensive Economic Partnership (RCEP) or the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) trade deals.

Of APAC respondents to the survey, 60% see their home region not only as a supply base but as an end market. Globally, 40% of respondents consider APAC a supply base and an end market.

Raman warns the signs are clear that in a fragmented world, global firms have been making changes to their heavily cost-optimised, one-size-fits-all networks, and now favour a mix of global, regional, or local elements.

“Investments into other parts of Asia - outside of China – coexist with expanded investments into developed markets as organisations take advantage of generous national/trade-bloc-level trade incentives,” she concluded.