An analysis of S&P 500 companies’ environmental, social and governance (ESG) reporting revealed that governance metrics comprised just 8% of all referenced metrics across industries.

Gartner’s analysis found that ESG reporting in many formats is becoming standard among most S&P 500 organizations. For example, 89% of companies issued reports that address environmental and climate change impacts.

But while 47% of organizations issued formal reports on organizational governance, actual metrics for tracking progress within governance-related topics, including topics such as executive pay and pay equity, made up just 8% of the total ESG metrics reported on by S&P 500 organizations.

“While it’s good to see that the vast majority of S&P 500 companies are formalizing ESG reporting, our analysis suggests that governance metrics are being overlooked in the face of pressing social and environmental issues,” said Matt Shinkman, vice president with the Gartner Risk and Audit Practice.

He cautioned that organizations that fail to adequately measure and communicate around issues such as pay equity and executive compensation could face activist shareholder pressure, reputational damage and other negative consequences.

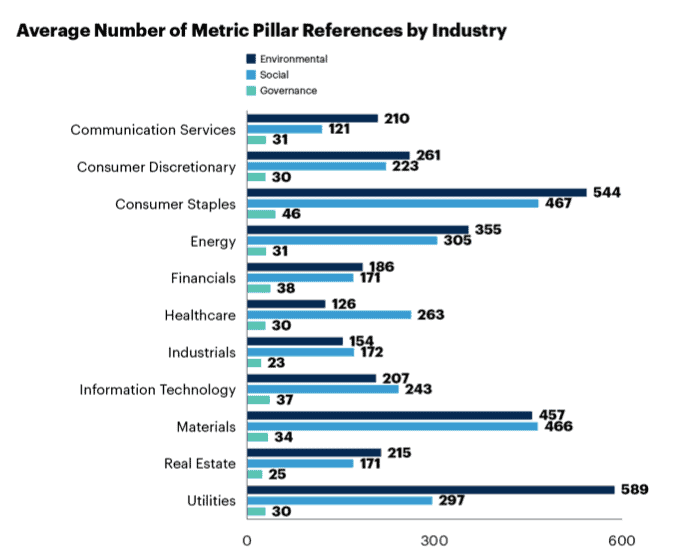

The analysis found that governance metrics were consistently under-referenced across industries. The consumer staples sector had the highest number of governance metrics referenced, while the industrials sector had the fewest governance metrics referenced (see Figure 1).

Figure 1. The average number of metric pillar references by industry

Shinkman added that there are various reasons that governance metrics could be lagging in ESG reporting across major organizations. The emergence of COVID-19 served as a forcing mechanism for companies to formally address health and safety protocols in a manner that likely would not have occurred without a global pandemic.

Gartner’s analysis revealed that “health and safety” metrics were the most often cited ESG metric by all companies, a sub-topic that belongs to the “social” pillar of ESG.

Industry-specific issues can also generate outsized reporting and metrics on a specific topic, such as the utilities, energy and consumer staples industries’ necessity to report on efforts related to reducing their climate impacts.

Social issues including diversity, equity and inclusion (DEI) had also risen in prominence in 2020, with shareholder, customer and media pressure for concrete improvements in this category.

Shinkman says that there are many pressing issues across the ESG spectrum. Organizations will not be able to sustain ignoring or giving only cursory attention to topics such as executive pay and pay equity indefinitely.

“Organizations should benchmark where they are on these issues now, and not wait for a headline event to force them into action overnight, as many had to do in 2020 related to improving their DEI metrics in the face of social justice protests across the globe,” concluded Shinkman.